Funds in Focus

Carmignac Sécurité: Letter from the Portfolio Manager

The Bond Market

Contrary to expectation, 2020 proved to be an extremely chaotic year. The ups and downs in the pandemic kept fixed-income markets on a roller-coaster ride and in utter uncertainty – until central banks and governments stepped in to give them crucial support, or rather life support. Despite recording significant declines when market liquidity dried up, closing off all avenues other than cash investments. When the time was ripe, we regained exposure first to quality corporate issuers who had experienced unwarranted selloffs, and subsequently to sovereign bonds from the eurozone periphery, particularly from Italy. The outlook for the latter has radically improved as a result of the epoch-making EU Recovery Fund and the ECB’s massive intervention. Our highly targeted exposure to specific corporate issuers in sectors badly battered by the pandemic also paid off.

In the fourth quarter, with the announced arrival of Covid-19 vaccines, risk assets continued to perform well in what turned out to be a less depressed economy than many had feared back in March (those fears being what motivated such huge fiscal and monetary stimulus programmes).

Likewise, large-scale central-bank intervention kept core interest rates from surging at an inopportune time

Germany’s 10-year yield stayed within a 14 basis-point range, from between –0.48%* and –0.64%*, before ending the quarter virtually unchanged at –0.55%*.

In contrast, Italy’s 10-year yield eased practically without interruption, shrinking from 0.87%* to 0.57%*. Portuguese, Greek and Spanish yields followed a similar pattern. Hopes for an economic upturn also led to a sharp increase in inflation expectations, though the realised inflation rate has strikingly failed to pick up. That increase, combined with what are still extremely low nominal yields, has driven real yields down and given rise in turn to hopes for resurgent GDP growth.

Though corporate credit experienced a mild swoon in October, it resumed its upward trajectory as spreads continued to narrow. The iTraxx Crossover Index fell from 345 to 238 basis points in the course of the fourth quarter. For now, the absence of large-scale bankruptcies and the average yields on corporate credit suggest that the public-health crisis hasn’t had, and won’t have, much economic impact, though that may be an overly sunny picture.

*Source: Carmignac, Bloomberg as of 31/12/2020. Performance of the A EUR acc share class

Portfolio Management

The movements we made in our portfolio during the fourth quarter were mainly driven by a desire to reduce risk. First of all, we scaled back the Fund’s overall modified duration by taking profits on UK gilts and shorting long-term US Treasuries (as the United States is once again a step ahead of Europe on the road to economic recovery). Second of all, we shorted countries with deeply negative real yields and whose central banks will likely be among the first to have to lift key rates – i.e., Norway, Poland and the Czech Republic.

-

We also reduced risk by taking profits on bonds from the eurozone periphery as credit spreads tightened. In Italy and Cyprus, we mainly wound down our holdings of long-dated paper.

Last of all, we reduced our overall credit allocation both by dialling back a few of our stronger convictions (e.g., Pemex, Ford and Carnival) and by buying protection.

-

Source: Carmignac, 31/12/2020

Investment Outlook

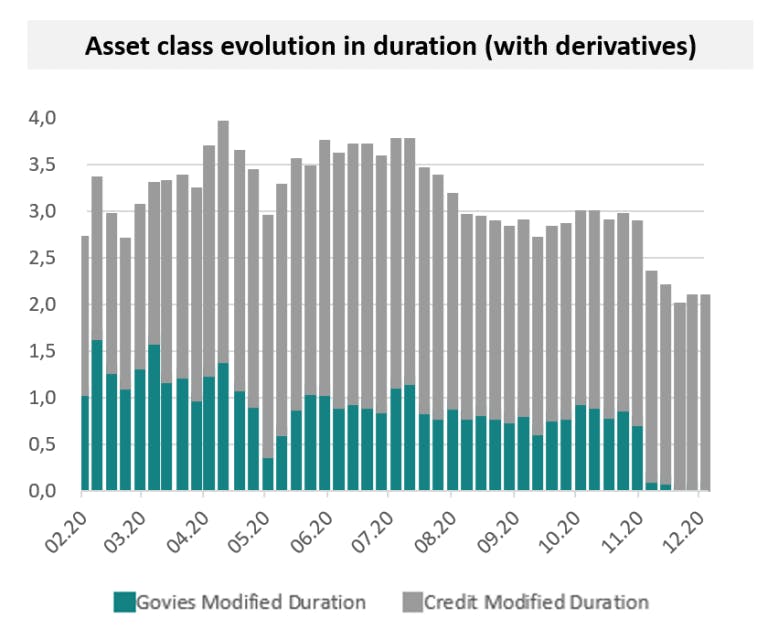

The Fund ended 2020 with total modified duration of 2 years, due almost exclusively to our corporate credit holdings, as our short positions on core sovereign bonds cancelled out our long positions on the eurozone periphery.

Our portfolio construction rests on the conviction that central banks will continue to expand their balance sheets, even if that expansion proves to be less dramatic than in 2020. With interest rates now rock-bottom, expanding the balance sheet is the only effective tool left to central banks. That said, bond markets tend to be more responsive to expectations of liquidity injections than to the injections themselves. This means that they probably have already priced in such monetary stimulus to a large extent. We therefore expect that, barring new developments, our portfolio will be characterised by fairly low duration, and made up primarily of short and medium-term maturities.

In corporate credit, technical factors admittedly still weigh heavily. The fact that the ECB holds 8.5% of Europe’s IG market has compelled investors to switch to lower-rated issues; volatility has subsided since Joe Biden's victory and the end of the Brexit saga; and central banks continue to provide unfailing support. And even if the dispersion observed in the credit markets still offers many investment opportunities, the current combination of negative yields and already tight credit spreads makes it particularly challenging. In addition, the resumption of lockdowns in Europe gives us little reason to expect a near-term end to the crisis which has led us to scale back our allocation and buying credit protection until we have more visibility on the evolution of the virus and the vaccination campaign.

Carmignac Sécurité AW EUR Acc

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

2024 (YTD) ? Year to date |

|

|---|---|---|---|---|---|---|---|---|---|---|---|

| Carmignac Sécurité AW EUR Acc | +1.69 % | +1.12 % | +2.07 % | +0.04 % | -3.00 % | +3.57 % | +2.05 % | +0.22 % | -4.75 % | +4.06 % | +2.34 % |

| Reference Indicator | +1.83 % | +0.72 % | +0.30 % | -0.39 % | -0.29 % | +0.07 % | -0.15 % | -0.71 % | -4.82 % | +3.40 % | +0.34 % |

Scroll right to see full table

| 3 Years | 5 Years | 10 Years | |

|---|---|---|---|

| Carmignac Sécurité AW EUR Acc | +0.36 % | +1.01 % | +0.71 % |

| Reference Indicator | -0.53 % | -0.48 % | -0.12 % |

Scroll right to see full table

Source: Carmignac at 28/06/2024

| Entry costs : | 1,00% of the amount you pay in when entering this investment. This is the most you will be charged. Carmignac Gestion doesn't charge any entry fee. The person selling you the product will inform you of the actual charge. |

| Exit costs : | We do not charge an exit fee for this product. |

| Management fees and other administrative or operating costs : | 1,11% of the value of your investment per year. This estimate is based on actual costs over the past year. |

| Performance fees : | There is no performance fee for this product. |

| Transaction Cost : | 0,24% of the value of your investment per year. This is an estimate of the costs incurred when we buy and sell the investments underlying the product. The actual amount varies depending on the quantity we buy and sell. |

Reference indicator : EuroMTS 1-3 years index (EUR). Performance of the A EUR acc share class. Past performance is not necessarily indicative of future performance. The return may increase or decrease as a result of currency fluctuations. Performances are net of fees (excluding possible entrance fees charged by the distributor).

Main risks of the Fund

INTEREST RATE: Interest rate risk results in a decline in the net asset value in the event of changes in interest rates.

CREDIT: Credit risk is the risk that the issuer may default.

RISK OF CAPITAL LOSS: The portfolio does not guarantee or protect the capital invested. Capital loss occurs when a unit is sold at a lower price than that paid at the time of purchase.

CURRENCY: Currency risk is linked to exposure to a currency other than the Fund’s valuation currency, either through direct investment or the use of forward financial instruments.

The Fund presents a risk of loss of capital.

![[Scale risk] 2/2 years_EN](https://carmignac.imgix.net/uploads/article/0001/11/a5355a3b50d44b6ada2b1a851cb9ec3213290a6c.png?auto=format%2Ccompress "[Scale risk] 2/2 years_EN")

* Risk Scale from the KIID (Key Investor Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time. A EUR Acc share class ISIN code: FR0010149120.

Carmignac Sécurité AW EUR Ydis

Recommended minimum investment horizon

Lower risk Higher risk

INTEREST RATE: Interest rate risk results in a decline in the net asset value in the event of changes in interest rates.

CREDIT: Credit risk is the risk that the issuer may default.

RISK OF CAPITAL LOSS: The portfolio does not guarantee or protect the capital invested. Capital loss occurs when a unit is sold at a lower price than that paid at the time of purchase.

CURRENCY: Currency risk is linked to exposure to a currency other than the Fund’s valuation currency, either through direct investment or the use of forward financial instruments.

The Fund presents a risk of loss of capital.