Flash Note

Why should we be interested in family firms?

- Published

-

Length

2 minute(s) read

Family businesses have long demonstrated their capacity to generate growth and profits. Their financial health and economic models enable them to be resilient over the long-term, even during periods of crisis.

What is a family business? Whether wholly or partially owned and directly or indirectly by a founder, a family or its descendants, for many people, family businesses are synonymous with small companies operating primarily on a local basis. The reality can be quite different, however.

In fact, some major international groups are also family businesses, such as global clothing sector leader Inditex (Zara, Massimo Dutti, etc.), Italian sports car manufacturer Ferrari, the German automotive group BMW, stainless steel producer ArcelorMittal, South Korean conglomerate Samsung, and even US retail giant Walmart. These family businesses employ millions and play a predominant role in global economic growth by contributing around 70% to global GDP1.

In fact, nearly four out of five companies worldwide are family businesses2. Present all over the world, operating in all sectors and of very different sizes, family businesses typically share common values: entrepreneurial spirit, independence, innovation, long-term vision and a desire to sustain the business. Furthermore, they offer genuine advantages for investors.

According to “Family 500”, our proprietary database, the average level of indebtedness is around three times lower than that of the average of other listed companies around the world. In contrast, their profitability is higher, with, for example, ROE (Return on Equity) – i.e. a company’s capacity to turn the money invested by its shareholders into profit – of 14% in 2019, compared with 12% for non-family firms.

Another advantage is their stability during times of crisis. For example, during the two major crises seen in recent years (2000 and 2007-2008), the family businesses’ profitability was significantly less volatile than that of other companies. Although family businesses’ ROE increased from 10.8% to 13.2% between 1997 and 2012, that of non-family businesses fluctuated erratically during the same period: 13.7% between 1997 and 1999; 8% in 2000-2002; 14% from 2003 to 2007; 4.6% between 2008 and 2009; and 13.4% in 2010-2012.

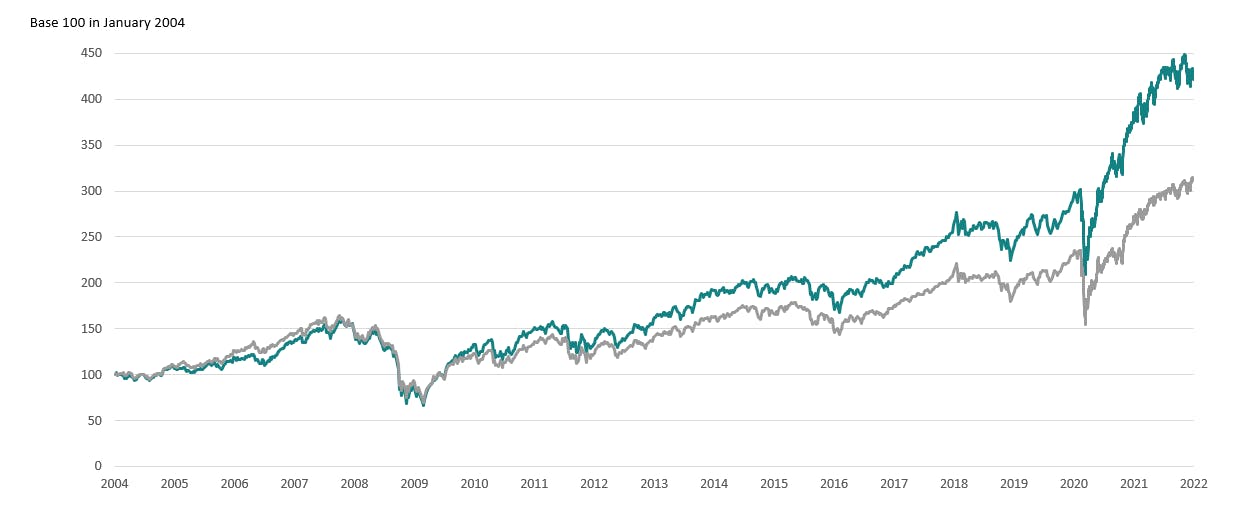

As a result, family businesses outperformed other publicly traded companies.

The market value of family businesses has more than quadrupled in 18 years, while that of non-family businesses has tripled over the same period

“The people leading these companies have a long-term vision and are risk averse because of the personal investment they have made in them, both in terms of time and money,” states Obe Ejikeme, portfolio manager at Carmignac. “This explains why these companies tend to be more resilient during difficult periods.”

On the other hand, the governance structure at these companies can be an area of weakness. This is particularly the case when it comes to establishing this governance structure or transferring a business to the next generation, as was brilliantly portrayed in the US TV show Succession.

“Succession planning is a key area of interest for us when we look at a family business,” explains Mark Denham, Head of the European Equities team at Carmignac. And portfolio managers can highlight the values shared between the family companies in which they can invest and Carmignac, which is wholly owned by its employees and the family of the same name.

Investors are wise to look into family businesses, given their capacity to create long-term value and to participate in the development of the local and global economy. They must be discerning, however, and carry out in-depth analyses.

“To invest in family businesses, knowing how to identify the best companies and being discerning is key,” emphasises Denham. “Diversification is just as important, not only in terms of sector but also geographical region or which generation is at the helm: first, second, third, etc.”

1UBS report, June 2019.

2Global Entrepreneurship Monitor, 2019-2020 Family Entrepreneurship Report, Babson Park, Donna J. Kelley, William B. Gartner, Mathew Allen.