Flash Note

Lessons from China: Exploring the great reopening

Each year, our emerging markets fund managers and analysts travel to the countries in which we invest. These visits are crucial. Not only for the team to meet the management of our current and potential portfolio companies but also to get a tangible picture of the day-to-day reality of the businesses (through visiting, manufacturing sites, for example) and to get local insight on the economic developments and major policies of the countries through conversations with local experts, consultants and residents.

Economy

Recovery led by local services

In China, zero-Covid restrictions really are over. Whether it is in small villages or big cities, life seems to be back to normal. Local consumption (services, hotels and restaurants) seems to have recovered with a strong pick-up in activity. There is evidence that consumption will be the main driver of recovery in 2023, with an expected rebound of more than 8% in 2023 after contracting last year.

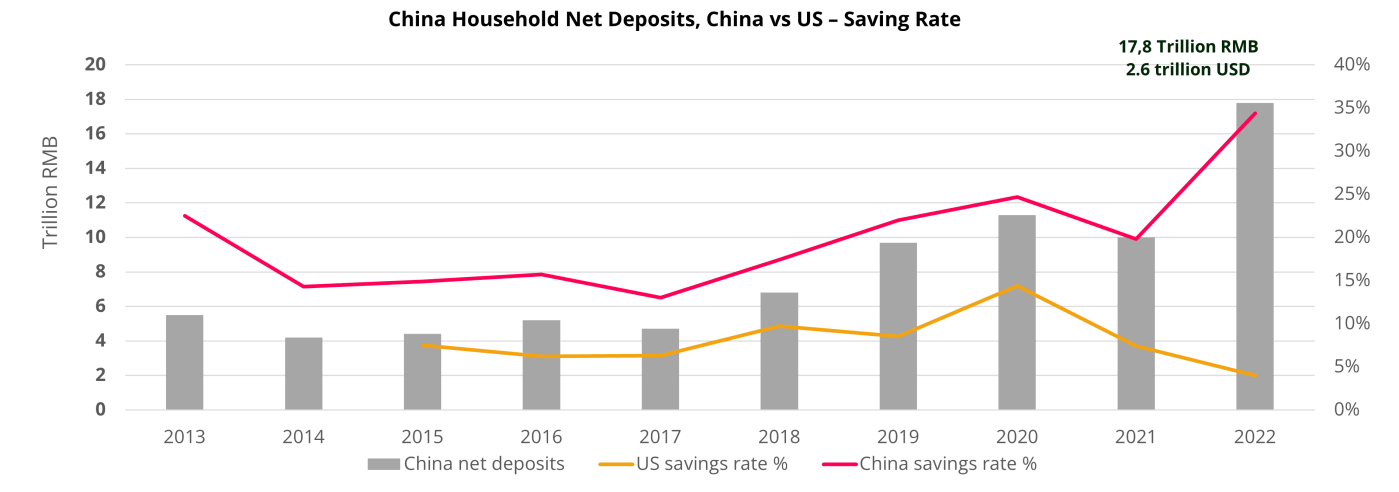

Nevertheless, the pandemic has significantly impacted the Chinese economy and society. We’ve witnessed a decline in employment and income, as well as a rise in household savings as people tried to preserve their financial stability in the face of uncertainty.

And despite the improvement following the reopening, Chinese consumers remain cautious and selective. Sales of high-ticket items have not really picked up. There is no “revenge spending”, and discretionary consumption has been slower than expected.

Real estate

Not a future growth engine

While it is too early to have a definite view on the housing recovery, there have been some improvements in data, notably, in home prices and sales picking up and government actions in providing funding, relaxing regulation, lowering mortgage rates. Secondary market transactions will likely post a decent rebound this year.

Despite these positive developments, the property market, in our view, isn’t a future growth engine for China. Factoring in the weaker primary market, property investments are likely to be down in 2023, even after a 10% contraction in 2022 .

Politics

Pragmatism prevails

We observed a rise in pragmatism from local governments when applying central government policies. This leads us to believe that local governments have learnt from past mistakes and will lead to more practical policies when managing local budgets and applying central government policies in their region.

On the national scale, China's new Premier, Li Qiang has sought to reassure the private sector and international business community of Beijing's pro-business stance, stressing the desire to create an atmosphere of respect towards entrepreneurs - a rare statement from a Chinese leader. He also affirmed that China will continue to rely on opening up (and reform) to achieve its long-run growth target.

In practice, this means further aligning with high-standard international business rules and improving public services to foreign enterprises. These announcements are very encouraging.

Society

Modernization boons

Despite three years of restrictions, it’s clear China did not slow down its urbanisation.

China’s rapid adoption of new technologies has provided a “leapfrogging” effect, making it one of the most developed countries in terms of digitalisation.

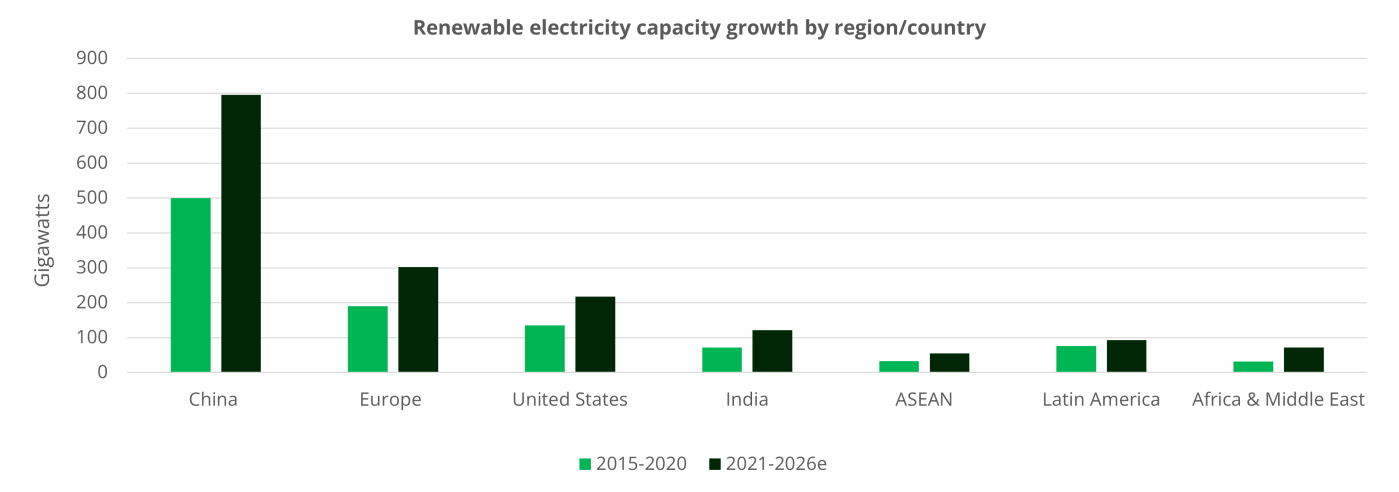

China has become the world leader in terms of renewable technology, outpacing others in the growth of electric power capacity from renewable technologies. This will lead to major long-term investment opportunities.

Common prosperity, often questioned in the West, is, in our view, positive for social stability and China’s path to sustainability, but some problems remain. Firstly, the high level of local government debt and secondly, no visible (effective) solution for China’s demographic pressure. Further, living and education costs remain high. And the tutoring sector reform has not produced the expected effect as parents are still paying much higher costs for one-to-one tutoring.

Geopolitics

Uncertainty ahead

While its clear the US and China will remain great rivals, with Chinese citizens expecting no “warming” in the relationship, the US-China decoupling looks structural and negative for China. There doesn’t seem to be a good solution for China’s semiconductor development and our Chinese trip did not give us a lot of comfort in that space.

Tensions with Taiwan are also a concern for China and global equities. Given the elevated geopolitical strains, Chinese equity risk premium will remain high and we choose to avoid Chinese companies that have a high level of exposure to such challenges (such as semiconductors and chip makers).

Chinese growth still outpaces

Despite some clear challenges, alongside India, China will still be the fastest-growing global economy this year with more than 5% growth (reinforced by the latest GDP data) and above all, a higher quality growth.

Moreover, after two years of sell-off, Chinese companies have attractive valuations, are buying back their shares, increasing dividends and as illustrated by recent announcements (Alibaba and JD.com splitting their business into several listed entities), trying to move in a direction of transparency, which is better in terms of cash flow generation.

The companies best positioned are those with good supply and demand dynamics in the domestic market, as well as companies able to “go global", as more Chinese companies try to reach international consumers.

While the great reopening will continue to see some bumps along the way, our experience in China has reinforced our conviction that there are many reasons to be positive – but selectivity remains essential.