Flash Note

A shift in market dynamics calls for an alternative approach

- Published

-

Length

4 minute(s) read

Now that inflation is back in the global economy, investors are facing a radically different landscape from the one experienced since the 2008 financial crisis. Over the past two years, yields across fixed income segments have experienced multiple-fold increases. Core government bond yields are now out of negative territory, those on emerging market bonds have risen by a factor of two (from 4.5% to nearly 9%), and those on European high yield indices have gone from 2.3% to more than 7% – a threefold increase. The negative correlation between bonds and equities, that diversified portfolios enjoyed for nearly 20 years, has come to an end.

And since the inflationary pressure will likely continue for at least the medium term, investors will have to find new ways of diversifying their portfolios.

Merger arbitrage strategy to diversify your potfolio

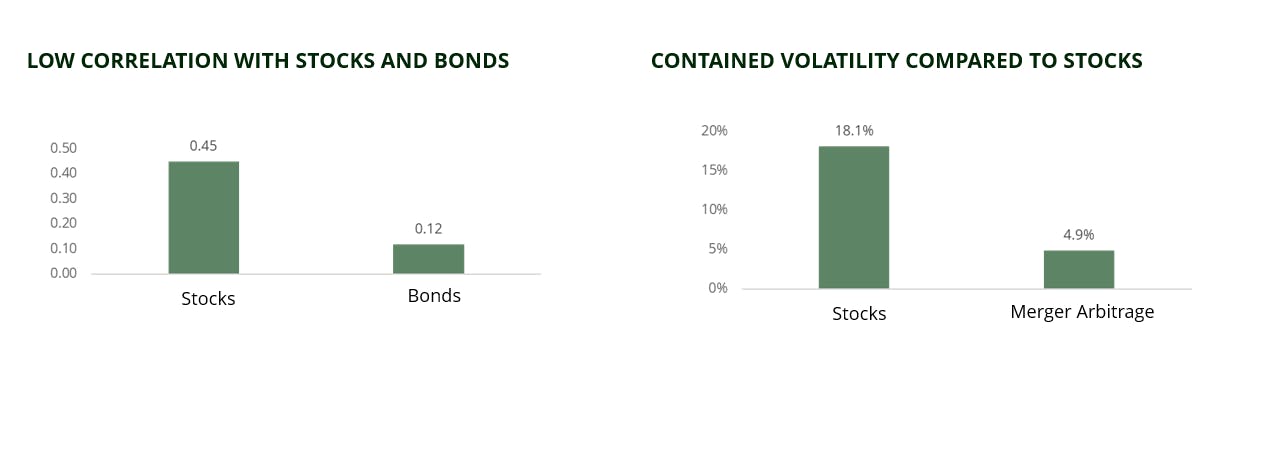

Merger arbitrage is an alternative strategy whose objective is to take advantage of price discrepancies, observed after the announcement of an M&A (Merger & Acquisition) transaction on a listed company. It is especially suited for current market environment, as it presents an effective hedge in rising rate or inflationary environment. The strategy often displays a lower volatility compared to stocks with low correlation with traditional asset classes such as equities and bonds.

Merger arbitrage strategies typically involve building a diversified portfolio containing 50–60 holdings, each in a company involved in an M&A deal. The main risk associated with this portfolio is idiosyncratic – the market risk has been replaced by deal-failure risk. In other words, whereas stock-price movements generally track the broader market, movements in merger arbitrage spreads follow their own dynamic that’s driven by the steps in the corresponding deal. That means merger arbitrage strategies are only weakly correlated with equity markets – and with bond markets, too.

For illustrative purpose only. The HFRI Merger Arbitrage Index is used as a proxy for the merger arbitrage universe.

Sources: Carmignac, Bloomberg at 30/06/2023.

Natural protection against high interest rates

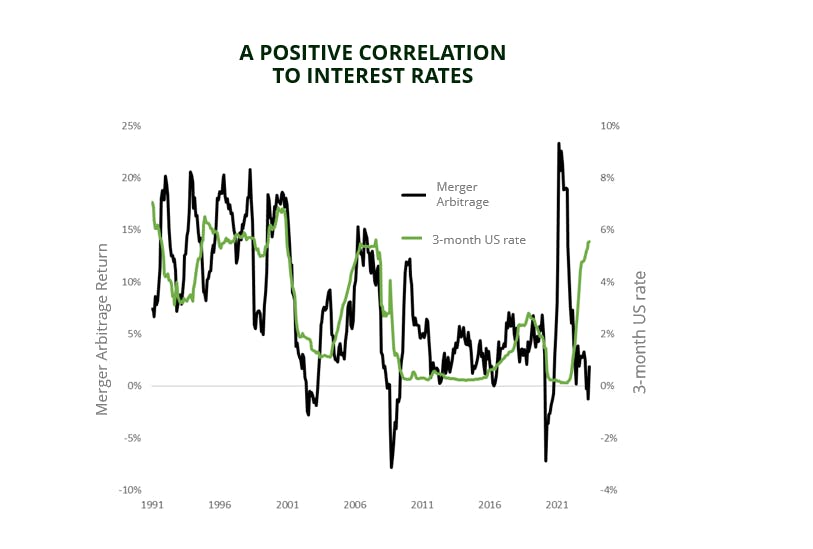

Merger arbitrage strategies are particularly well-suited to times of rising interest rates. Since the risk-free rate is one of the two components of a merger arbitrage spread, increases in this rate – i.e., the short-term interest rate – will automatically push up the expected return on a merger arbitrage strategy for the same level of risk.

This pattern appears to hold over extended periods of time. For instance, merger arbitrage spreads followed movements in interest rates between 1990 and 2008: they declined after the dot-com bubble burst in 2001 and rose during the 2004–2007 economic recovery. But the correlation was undone by the 2008 financial crisis and the ensuing era of 0% interest rates engineered by central banks.

For illustrative purpose only. We use the HFRI Merger Arbitrage Index to describe the Merger Arbitrage universe. Source: Carmignac, Bloomberg. Data as of 30/06/2023.

Merger arbitrage at Carmignac

At Carmignac, we’ve been expanding our alternative-investment capabilities for years and currently manage nearly €2 billion in this asset class. We formed a merger arbitrage team and appointed Fabienne Cretin-Fumeron and Stéphane Dieudonné as Fund managers. This move came in response to growing demand from investors seeking to diversify away from conventional asset classes and into those with reduced volatility and uncorrelated returns.

We launched two merger arbitrage Funds: Carmignac Portfolio Merger Arbitrage, which has a defensive profile and 2%–4% expected volatility; and Carmignac Portfolio Merger Arbitrage Plus, which is more dynamic and has 5%–7% expected volatility. These funds aim to seize M&A opportunities in the main developed countries. They’re both classified as Article 8 under the SFDR and are open to professional and retail investors in several European countries.

Carmignac Portfolio Merger Arbitrage A EUR Acc

Recommended minimum investment horizon

Lower risk Higher risk

EQUITY: The Fund may be affected by stock price variations, the scale of which is dependent on external factors, stock trading volumes or market capitalization.

ARBITRAGE RISK: Arbitrage seeks to benefit from such price differences (e.g. in markets, sectors, securities, currencies). If arbitrage performs unfavorably, an investment may lose its value and generate a loss for the Sub-Fund.

RISK ASSOCIATED WITH THE LONG/SHORT STRATEGY: This risk is linked to long and/or short positions designed to adjust net market exposure. The fund may suffer high losses if its long and short positions undergo simultaneous unfavourable development in opposite directions.

LIQUIDITY: Temporary market distortions may have an impact on the pricing conditions under which the Fund might be caused to liquidate, initiate or modify its positions.

The Fund presents a risk of loss of capital.

Carmignac Portfolio Merger Arbitrage Plus A EUR Acc

Recommended minimum investment horizon

Lower risk Higher risk

EQUITY: The Fund may be affected by stock price variations, the scale of which is dependent on external factors, stock trading volumes or market capitalization.

ARBITRAGE RISK: Arbitrage seeks to benefit from such price differences (e.g. in markets, sectors, securities, currencies). If arbitrage performs unfavorably, an investment may lose its value and generate a loss for the Sub-Fund.

RISK ASSOCIATED WITH THE LONG/SHORT STRATEGY: This risk is linked to long and/or short positions designed to adjust net market exposure. The fund may suffer high losses if its long and short positions undergo simultaneous unfavourable development in opposite directions.

LIQUIDITY: Temporary market distortions may have an impact on the pricing conditions under which the Fund might be caused to liquidate, initiate or modify its positions.

The Fund presents a risk of loss of capital.