Fund Focus

Carmignac P. Unconstrained Euro Fixed Income: the Fund Manager’s thought

Since March 10th, 2021, the new name of Carmignac Portfolio Unconstrained Euro Fixed Income is Carmignac Portfolio Flexible Bond.

The bond market today

After the disruption caused in the first half of the year by the Covid-19 outbreak, the third quarter seemed more placid. Yet it also saw quite a few developments with an impact on bond-market behaviour as almost all market segments booked substantial gains over the period.

-

The Covid-19 pandemic so dramatically affected global economic activity that it drove government and monetary institutions across the board to provide large-scale support.

-

In July, for example, the EU at last agreed on a Recovery Fund that set the stage for ambitious fiscal stimulus programmes. With the number of persons infected by Covid-19 worldwide rising by the end of summer, governments began preparing for a probable second wave, adopting protective policies that would impact the economy, despite the publication of better than expected economic indicators and some progress on vaccines.

US fixed income has in particular felt the impact of the recent policy shift at the Federal Reserve. To help achieve his inflation and job-growth targets, the Fed would now tolerate brief phases of economic overheating and therefore temporary increases in the inflation rate to over 2%. This announcement was enough to steepen the yield curve and strongly support Inflation-linked securities.

Another factor affecting US fixed income has been the country’s feverish political climate with no agreement reached on a new stimulus bill and no clear outlook on the upcoming presidential election. Emerging-world bond markets showed dispersion, but overall credit risk is on the mend being buoyed by US dollar depreciation and by the rebound in commodities.

Portfolio allocation

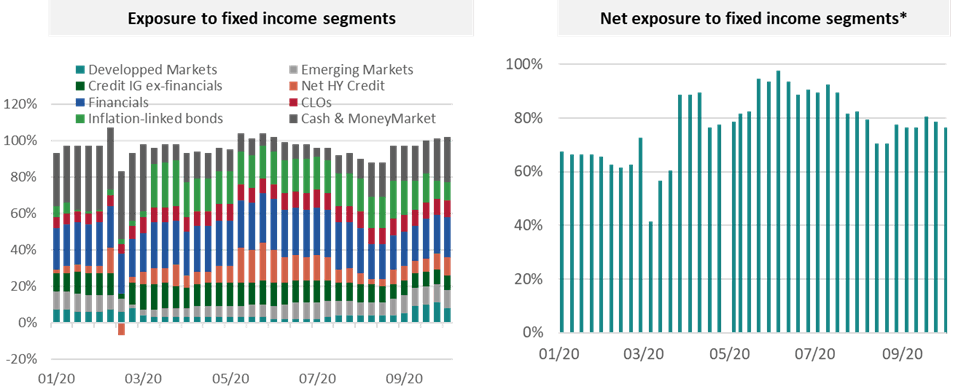

The effects of the economic downturn have been offset by stimulus policies introduced around the world, leading us to invest heavily during the second quarter in various parts of the credit space. By early July, corporate credit accounted for 64% of our fixed-income allocation. With central banks engaged in an increasingly pronounced economic support drive, we took inflation-linked bonds to 19% of our portfolio at the start of July to benefit from rising inflation expectations and falling real interest rates. We thus entered the third quarter with 91% exposure to the fixed-income market and negligible cash holdings – a sign of the many opportunities the market had to offer at that point.

*Investments – hedging via derivatives – cash & cash equivalents

Source: Carmignac, 09/10/2020

Buoyed by support from governments and central banks, high-risk credit spreads tightened fast, especially in high-yield (+3%) and subordinated financial debt (around +4%) markets. This convinced us to take profits and scale back our exposure to high-yield credit to an exposure at around 9% now.

We have nonetheless left corporate bonds at nearly 50% of our portfolio with two main convictions:

- Some issuers whose businesses took a direct battering from the Covid-19 outbreak (e.g., certain carmakers, aircraft manufacturers, etc.) with significant performance potential.

- Financial bonds, particularly the more junior issues, as they are receiving extremely generous support from central banks and are still benefiting from their efforts over the past several years to clean up their balance sheets.

This ongoing monetary policy easing should sustain low volatility in markets – a plus point for carry strategies. With that in mind, we have made a large investment in Italian government paper (9%), given that political risk is now off the country’s medium-term agenda.

During the quarter, we raised our exposure to emerging-market bonds focusing now on what are the team’s major convictions: the Mexican oil company Pemex, Romania and the Russian fuel and energy consortium. We have been especially active in the market for inflation-linked bonds and have now a substantial 10% exposure to European and US inflation-linked bonds.

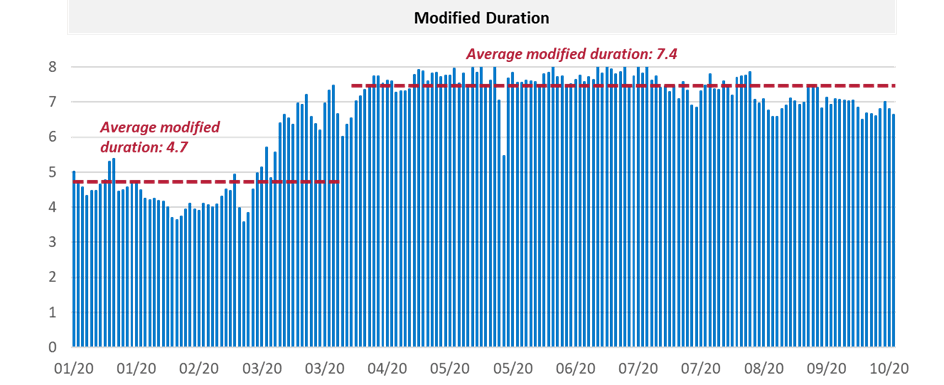

Portfolio duration

During the quarter, we maintained our very high duration between 6.5 and 8. In September, we began mildly reducing our overall modified duration, keeping it below 7 years.

Source: Carmignac, 30/09/2020

Past performance is not a reliable indicator of future performance. Performances are net of fees (excluding applicable entrance fee due to the distributor). The return may increase or decrease as a result of currency fluctuations).

We maintain a high duration via hold large positions on the US and eurozone yield curves, and to a lesser extent and for diversification purposes on Australian and UK gilt yield curves, to take advantage of extremely dovish monetary policies.

The second case for maintaining high duration is that it allows us to protect a portfolio heavily invested in corporate bonds in case the economic landscape deteriorates. However, there are also yield curves on which we have opted for negative duration, for example in Hungary and the Czech Republic.

Fund performance

In the quarter, Carmignac Portfolio Unconstrained Euro Fixed Income returned +2.86% (A share class EUR Acc) versus +1.53% for its reference indicator (ICE BofA Euro Broad Index). Practically all the strategies we pursued made a positive contribution to the Fund’s performance. Corporate credit – with differentiated positioning in high-yield, investment-grade and financial bonds – lifted our return by 187 basis points.

We also booked positive results in government bonds from both the developed world (Italy) and the emerging world (mainly Romania). We also gained performance from our exposure to US and European real rates. Regarding duration management, we have mainly benefitted from our Australian bonds.

Carmignac Portfolio Flexible Bond A EUR Acc

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

2024 (YTD) ? Year to date |

|

|---|---|---|---|---|---|---|---|---|---|---|---|

| Carmignac Portfolio Flexible Bond A EUR Acc | +1.98 % | -0.71 % | +0.07 % | +1.65 % | -3.40 % | +4.99 % | +9.24 % | +0.01 % | -8.02 % | +4.67 % | +2.10 % |

| Indice di riferimento | +0.10 % | -0.11 % | -0.32 % | -0.36 % | -0.37 % | -2.45 % | +3.99 % | -2.80 % | -16.93 % | +6.82 % | -0.36 % |

Scorri a destra per vedere la tabella completa

| 3 anni | 5 anni | 10 anni | |

|---|---|---|---|

| Carmignac Portfolio Flexible Bond A EUR Acc | -0.40 % | +2.19 % | +1.03 % |

| Indice di riferimento | -4.33 % | -2.69 % | -1.47 % |

Scorri a destra per vedere la tabella completa

Fonte: Carmignac al 28/03/2024

| Costi di ingresso : | 1,00% dell'importo pagato al momento della sottoscrizione dell'investimento. Questa è la cifra massima che può essere addebitata. Carmignac Gestion non applica alcuna commissione di sottoscrizione. La persona che vende il prodotto vi informerà del costo effettivo. |

| Costi di uscita : | Non addebitiamo una commissione di uscita per questo prodotto. |

| Commissioni di gestione e altri costi amministrativi o di esercizio : | 1,20% del valore dell'investimento all'anno. Si tratta di una stima basata sui costi effettivi dell'ultimo anno. |

| Commissioni di performance : | 20,00% quando la classe di azioni supera l'Indicatore di riferimento durante il periodo di performance. Sarà pagabile anche nel caso in cui la classe di azioni abbia sovraperformato l'indice di riferimento ma abbia avuto una performance negativa. La sottoperformance viene recuperata per 5 anni. L'importo effettivo varierà a seconda del rendimento del tuo investimento. La stima dei costi aggregati di cui sopra include la media degli ultimi 5 anni o dalla creazione del prodotto se inferiore a 5 anni. |

| Costi di transazione : | 0,38% del valore dell'investimento all'anno. Si tratta di una stima dei costi sostenuti per l'acquisto e la vendita degli investimenti sottostanti per il prodotto. L'importo effettivo varierà a seconda dell'importo che viene acquistato e venduto. |

Carmignac Portfolio Flexible Bond

TASSO D'INTERESSE: Il rischio di tasso si traduce in una diminuzione del valore patrimoniale netto in caso di variazione dei tassi.

CREDITO: Il rischio di credito consiste nel rischio d'insolvibilità da parte dell'emittente.

CAMBIO: Il rischio di cambio è connesso all'esposizione, mediante investimenti diretti ovvero utilizzando strumenti finanziari derivati, a una valuta diversa da quella di valorizzazione del Fondo.

AZIONARIO: Le variazioni del prezzo delle azioni, la cui portata dipende da fattori economici esterni, dal volume dei titoli scambiati e dal livello di capitalizzazione delle società, possono incidere sulla performance del Fondo.

L'investimento nel Fondo potrebbe comportare un rischio di perdita di capitale.